What is dilution?

TLDR: Dilution is the reduction in the ownership percentage in a certain company as an effect of the issuance of shares.

Dilution refers to the reduction of an individual shareholder\’s ownership percentage in a company as a result of the issuance of new shares. In the context of startup investing, dilution can occur when a company raises capital through the sale of additional shares to investors. This can be done through a variety of means, such as issuing new shares in exchange for cash or issuing shares to employees as part of a compensation package. Dilution can also occur when a company issues new shares to acquire other companies or as a result of stock splits. While dilution can dilute the value of an individual shareholder\’s stake in a company, it can also provide the company with much-needed capital to fund its operations and growth.

How to calculate dilution?

There is a number of calculations to make before getting your final percentage of dilution. Let\’s work them out with an example.

Let\’s say you are the only owner of a company and you own 1000 shares. What happens if you issue 100 more shares?

The new total number of shares is 1000+100 = 1100 shares. You own 91% (1000 / 1100) and the buyer of the newly issued shares owns 9%.

But what is the formula behind the dilution calculation?

Continuing the example from above, you now own 91% of the company. What\’s the dilution? It is 9%.

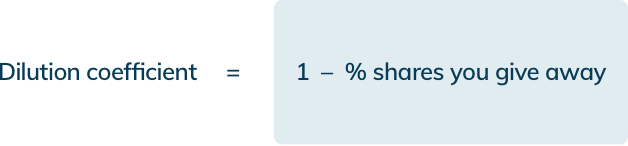

To calculate this, you first need to calculate the dilution coefficient.

The number of shares you give away in the example is 9%. So this is what the calculation would look like

In the previous case, there is only one owner of the company. But what happens if there were two initial owners of the company and new shares are issued?

Let\’s take the case when only one of the owners buys the shares. As above, we have 1000 shares in total. Each owner has 50% of the shares, which is 500 shares respectively.

100 more shares are issued, which brings the total amount of shares to 1100. Post issuance, one of the owners has 600 shares and the other has 500 shares, so 54,54% and 45,45% respectively.

In this case the formula for the dilution coefficient is slightly adjusted and it goes this way

Following the formula, the calculation looks like this:

This is the dilution calculation for the person who buys the additional shares, assuming that he buys them all.

If we talk about the shareholder that doesn\’t buy any of the new shares, his situation doesn\’t change.

Prepare yourself for fundraising with a clear and transparent Startup Valuation Report

What ownership can you expect in startups?

Startups typically require multiple rounds of fundraising—from inception until the company reaches positive cash flow. Generally, this means raising new rounds every one to two years, progressively at higher valuations to minimize dilution. However, even with strategic fundraising, dilution remains a reality.

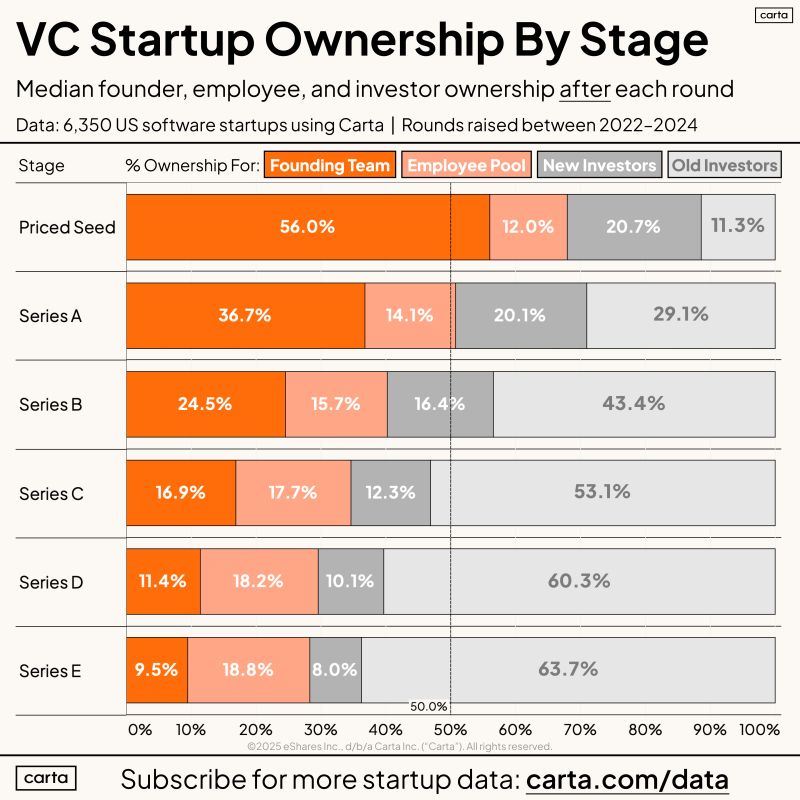

According to data from Carta, after completing a Series E funding round, the average founding team owns about 9.5% of the company. Individual founders typically end up holding less than 10% equity at this stage, although exact ownership percentages vary significantly based on the number of founders and the specific industry.

Industries that are highly capital-intensive (like hardware or biotech) tend to dilute founders more aggressively, as the ongoing need for substantial capital reduces the founders\’ share more rapidly. Conversely, less capital-intensive sectors (like SaaS or software) often allow founders to retain higher percentages of ownership over time.

Ultimately, the goal of managing dilution isn\’t simply to preserve maximum equity—it’s to balance founder incentives with investor expectations, ensuring that founders remain highly motivated while raising sufficient capital to maximize the company\’s odds of success. For a more comprehensive guide on typical dilution by stage, check out this article: Equity Percentages to Offer Investors at Different Stages

Why would you be subject to dilution?

There are three occasions when you issue shares:

1| Raising capital

When you are raising capital, you give away equity. This is the typical case and it is identical to the example above.

2| ESOPs, Stock options, RSU, warrants, etc..

When compensating employees, equity related compensation can be a great tool in a founder\’s arsenal (more here). Startups normally dedicate part of their equity to this purpose in what is called an Option Pool. Pool range normally from 10 to 20% but can be tipped up as the company grows. Shareholders should be aware of the dilution caused by equity compensation of employees and key people.

3| SAFEs and Convertible debt

In this case, debt holders will convert to shareholders at a trigger event, usually a funding round or an exit. Hence, this causes dilution for the initial shareholders.

There are other situations when a company issues shares and is subject to dilution, but these are the main three.

The last two types of securities signal to investors that dilution will happen at a future event. However, they are interested in finding out what exactly the dilution is prior to committing to invest. This is why some contracts ask for the shares on a fully diluted basis.

What\’s a “fully diluted basis”?

Let\’s say that you own 50% of the shares of a company and the other 50% belongs to another shareholder. There is also a person who is holding a stock option.

Stock options usually refer to a specific number of shares, which means that at the time that the option is exercised, a certain amount of shares will be issued.

“On fully diluted basis” means that you need to calculate how much you are going to own at the time the options is exercised. You can do that by subtracting the dilution you are going to get at the issuance of shares from the amount of shares you own today.

What usually happens when you are raising capital from a VC firm is that you are issuing shares for them, but you will also issue some additional equity. That ranges between 5-10%. You will allocate these shares in a separate entity – for instance, foundation or an escrow. These shares will be reserved for securities such as employee stock options or convertible debt.

The reason why you do that is that makes it easier to discuss equity stakes on a fully diluted basis. This amount of shares might never be used entirely. But on the plus side, even though they are shares with voting rights, they are controlled by the company. So they don\’t impact the voting process.

Calculating the dilution for stock options is relatively easy, because you know the exact amount of shares that are going to be issued. However, calculating dilution for convertible debt is a bit more difficult. In this case the number of shares at conversion will be determined by the valuation at the trigger event.

To make the dilution calculations you take the worst case scenario – you assume that the debt holders will convert at the cap. Since the cap is the maximum, so you can already calculate the maximum number of shares that will be issued.

What about you? What is your experience with dilution? Did you have any difficulties or were you prepared to talk about it during investment negotiations? Let us know in the comments!